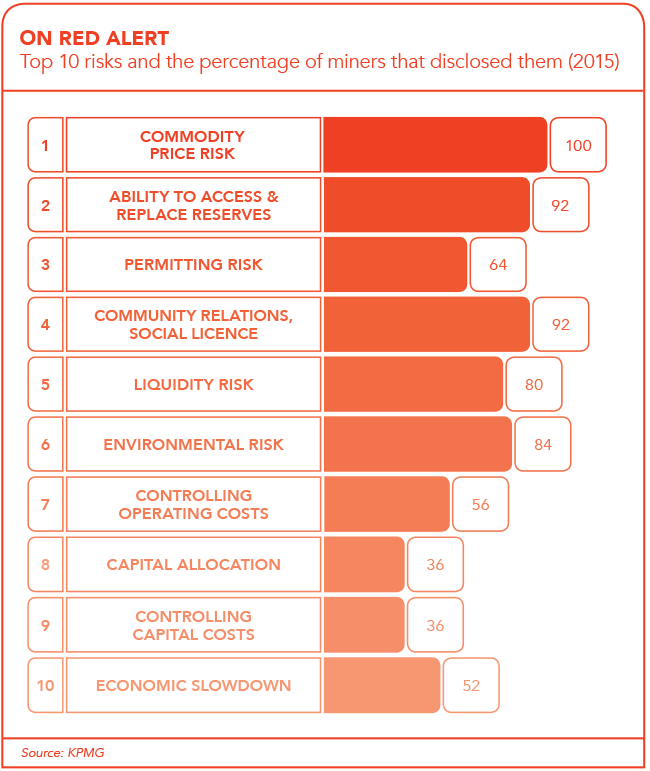

Regardless of what ore is mined or the methods used to extract it, or even the country in which operations take place, the mining business is fraught with risks, ranging from low level to high, going as far as loss of life and early mine closure. Indeed, business risks exist throughout the full life cycle of a mining operation, including transportation, construction, development, mining, processing and rehabilitation closure. Labour and strike action, changing legislation and accidents are also considerations.

Given this, mining insurance is a serious and vital consideration – one that also comes with a fairly high price tag. It is, however, a complex specialist area, as the risks associated with mining can be tough to place in the insurance market. After all, mining can generate some huge and high-profile losses. The insurance market does, however, provide a comprehensive selection of risk products well suited to the industry, and mining companies are taking full advantage of this.

When looking for insurance products, mining companies should approach brokers and service providers as early as possible – from the feasibility stage, according to Debbie Geraghty, regional manager of Marsh Africa. It is also a condition of the granting of mining rights that any closure guarantees be submitted to South Africa’s Department of Mineral Resources (DMR) beforehand.

The process of obtaining insurance generally begins with a risk assessment. ‘Assessors do a report describing the mine, the nature of operations, and the risk factors. Then they work out what the maximum foreseeable loss is, and use this to determine the limit the mine would require in terms of its insurance policy. It’s scenario based.’

Geraghty adds that mining companies should carry out professional valuations to ensure they are not underinsured. ‘The business interruption policy is also arranged on a declaration basis, usually with a 25% price cap to allow for fluctuations in mineral prices and rand/dollar exchange rate,’ she says.

Various mining exclusions have come up over the years, Geraghty further explains, with an example. ‘Following a collapse, the replacement of the shaft infrastructure is covered [but] the cost of re-digging the main shaft will not be covered.’

Marsh Risk Consulting (MRC), a consultancy within Marsh, has access to risk surveys and mining industry claims data and has created an industry-wide commodity-tailored set of benchmarks. MRC has invested heavily in developing risk assessment and benchmarking methodology and tools, including the Marsh Mining Risk Index (MMRI), through which realistic, expected and maximum foreseeable loss scenarios can be identified and clearly illustrated, to guide insurance decisions and risk-mitigation measures.

Recently released for local use, the MMRI enables data-rich reporting that includes a risk index to enable effective translation of risks to underwriters; benchmarking against relevant mines and processes; and links to loss estimates reflective of industry claims experience.

Analysis and deliverables are enhanced by other MRC specialties, such as tailings and machinery risk solutions, business continuity management and valuations.

While many risks can be insured, others are uninsurable.

Products available from the insurance market include asset and business interruption cover, which covers the loss of profit during the interruption period; liabilities cover, such as injury or damage to third parties; incidental cover, including motor, personal accident and crime cover; and closure or rehabilitation guarantees.

According to Geraghty, labour unrest that results in physical damage to assets is covered, and if the DMR closes a mine due to a fatality and there was physical damage to property, cover will be provided while the mine is closed.

There is, however, no cover available for changes in legislation or forex fluctuations above the 25% margin allowed.

Another relatively new addition to the risk space is cybercrime. According to AIG EMEA Cyber, ransomware and cyber extortion have become one of the fastest-growing sources of data loss for organisations – both large and small. From a severity perspective, business interruption and data breach will continue to be significant drivers of loss now and into the future, AIG stated in a recent cyber risk report.

Almost all companies handle both personal and corporate data daily, from identity numbers and employee profiles, to credit card details, sensitive demographic information, customer lists, budgets and marketing plans. Should this data fall into the wrong hands or enter the public domain, very real liabilities exist for the company whose defences were breached.

In mining, the situation is no different, as plenty of sensitive information is handled on a daily basis. There is also the risk of someone gaining remote access to the machinery and equipment on a mine by hacking into a system.

Rene Pillay, internal audit vice-president at Sibanye Gold, says that cyber insurance is a fairly new area of concern for the company – one that is still being explored and understood. ‘Traditional policies cover infrastructure, devices, laptops and so on, but we realised that we pay people, we have bank accounts, we upload to banking systems… Suddenly cyber has become important,’ she says.

‘The cyber space evolves very quickly and you have to keep pace. Having cyber insurance means we don’t have to manage a breach on our own. It’s a way to mitigate against risks. The insurance covers us should we have a breach. We can then remediate.’

According to Roxanne Griffiths, underwriting manager (financial lines) at AIG, product-buying patterns for cyber risk insurance have changed from reactive to preventive.

‘Boards of directors are now more focused on how they can prevent an attack from occurring and mitigation, as opposed to being able to respond,’ she says.

In this regard, AIG has compiled a host of value-added benefits for its clients through a suite of risk consultation and prevention services. These include the AIG CyberEdge mobile app (which provides clients with up-to-date global cyber breach information and news); IntelliShun (a global threat intelligence tool); and an infrastructure vulnerability scan, powered by IBM.

K2 Intelligence also works with clients to keep them current with the latest chatter in the ‘darknet’ about their entity, says Griffiths.

Use of vendors is also becoming increasingly important, she adds. ‘AIG has partnered with global forensic and legal response advisers who are best equipped to assist our clients in the event of a threat,’ she says.

‘Time is of the essence when a breach occurs, and having a response plan in place with access to third-party vendors will help clients efficiently and cost-effectively respond to – and recover from – a breach.’

The insurance offering is also changing, she adds, whereby cover includes both first-party and third-party loss, use of vendors and business interruption cover.

In addition to cyber insurance, Pillay says other areas of concern include directors’ and officers’ liability, bullion and project insurance. She adds that insurance forms a part of the company’s risk management area. ‘We look at the options for managing risks and one of the options is to transfer the risks out. Those areas where we transfer the risk are mainly under our business interruption and gross profit.’

Sibanye uses a broker to advise on available insurance options, according to Pillay, and the company makes use of different insurers for different reasons. They also undertake independent assessments of the company’s assets for valuations every year. ‘It’s a valuation provided by an independent party so that we are not over- or under-insured,’ she says.

Operating in Africa comes with its own set of risks – one that overseas markets don’t always understand, says Pillay. ‘It’s really about telling them that we can – that we are managing the risk of operating in South Africa,’ she says.

‘Most of our insurers are overseas, so we get a lot of questions. Overseas, they have exposure to open-pit mines, where we have deep-level, underground mines. We have to make them understand our business. When we’ve had an insurer come to South Africa for a visit, we’ve taken them underground, taken them to visit a mine and see what’s happening, so that they can relate to what we are saying. This has helped their understanding.’

For mining companies moving into Africa, Geraghty explains that the cover required is largely the same, except that in some countries, political risk cover might also be required. While companies still need to insure their assets, they often use contractors, who would have their own insurance.

‘It’s more the expropriation of the assets, especially the mobile equipment,’ according to Geraghty, adding that in her experience, a lot of international companies operating in Africa place their risks and insurance in the South African market, and do their servicing from the Marsh Africa network.

In lieu of the varied risks that can be encountered by mining companies, the general rule of thumb is that where cover is available, it should be purchased to protect to the maximum levels affordable.