In the 1970s, the continent’s states were world-leading producers of some rare earth elements (REE). Over the years, however, Africa’s producer role has been almost entirely eclipsed by China, as have rare-earth producers in the US and elsewhere. Back then, REE barely registered on the radar of the broader mining industry and its investors. This group of elements now occupies an increasingly central place in the high-tech manufacturing arena, and the need for diversified supplies – at dependable prices – will continue to grow.

During the last commodities boom, concerns about China’s dominance of the supply drove a storm of speculative investment into African rare-earths exploration, with the expectation that new discoveries would reshape the dynamics of global supply. But China kept meeting global demand, and these investments often foundered, or exploration didn’t take place in any serious way.

In recent years, attention has often been focused on problems with the production of related materials in Central Africa – the tantalum and niobium that are used widely in mobile-phone technologies – where failed supply chains have fuelled labour exploitation, pollution and local warlords. But REE represent a far broader range of materials distributed across the continent.

The search continues for good deposits outside of China, and African states have hosted some important recent developments.

The rare earths are a diverse (and hard to pronounce) set of elements – and usually divided into two groups. There are the ‘light’ rare earths, comprising lanthanum, cerium, praseodymium, neodymium, promethium and samarium. Then there are the more valuable ‘heavy’ rare earths – europium, gadolinium, terbium, dysprosium, holmium, erbium, thulium, ytterbium and lutetium. Few of these are actually ‘rare’ in terms of absolute scarcity – they are widely distributed, and instead their names come from the difficulty in finding deposits that can be mined economically. This usually means clay-type deposits, where REE can be separated easily from host minerals.

In terms of use, REE have buyers across all sectors of high-tech manufacturing. Some, such as cerium, are common in most deposits, but have relatively little value. Cerium is used for making LED lighting, along with yttrium. Neodymium and praseodymium, on the other hand, are pivotal elements in the production of high-performance magnets, used in drive trains for electric vehicles, as well as in wind turbines, and in audio technology. Many REE find their way into mobile phones, and they also play a central role in military equipment – hence the strategic importance in securing supplies from different sources.

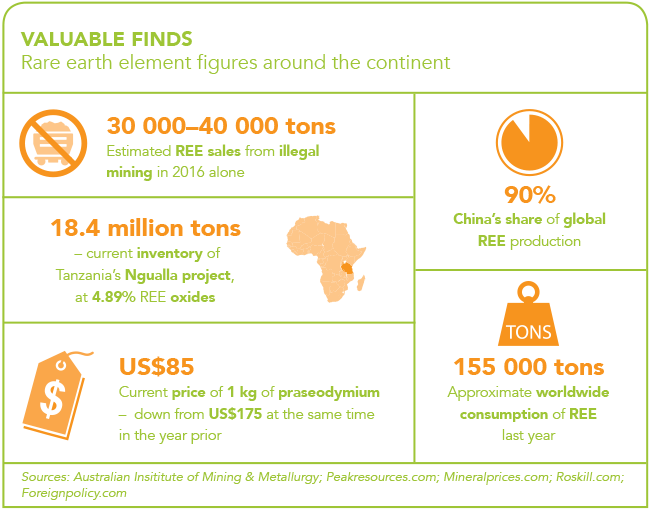

Even before 2010, China dominated rare-earths production, with the vast ionic clay deposits of the Bayan Obo mining district in Inner Mongolia. This was a cause of concern to some governments and sectors, notably military manufacturing, but the implications had not sunk in for smaller investors. In 2010, however, China cut production of REE by 40% – squeezing global supplies and sending prices skywards – accompanied by consolidation of its domestic producers and an attempt to reduce illegal rare-earths production and further constraining supplies. The moves gave rise to an explosion of REE exploration and investment elsewhere in the world – including in many African states – and several large alternative REE sources were en route to long-term production in the US, Australia and across Africa.

Since then, however, China has re-asserted its dominance. Its domestic illegal REE production has again expanded, driving prices back down and undermining the business case for many mines elsewhere. Two of the leading North American rare-earths producers filed for bankruptcy this past year – Molycorp Inc (with its Mountain Pass mine in California), and Canada’s Great Western Minerals (with assets in South Africa and elsewhere) – having spent years and millions trying to develop and sustain their projects.

According to minerals research firm Roskill, China was responsible for 90% of global REE production in 2016. A further 8% came from Australia, where Lynas Corporation has been able to survive falling prices with production from its Mt Weld mine. Total worldwide consumption of rare earth oxides was around 155 000 tons in 2016 – a tiny volume compared with other mineral commodities, and more than 60% of this consumption took place within China.

With only 2% of production located outside China or Australia, it’s clear that almost all industrial users – including the US – remain dependent on China and its policy decisions. As analysts writing for the Australasian Institute of Mining and Metallurgy recently noted: ‘Chinese dominance is not only a matter of reserves, but rather the result of a carefully crafted long-term strategic plan.

The Chinese strategy, combined with lax environmental regulations, tax rebates and cheap labour, quickly yielded results and operations in China were able to scale up in a relatively short period of time. There was also significant effort to develop the intellectual capital needed for the REE industry in China. This is exactly the intellectual capacity that the rest of the world is now lacking.’

The current picture looks grim for firms wanting to produce REE elsewhere though some African projects have the potential to compete. In north-west Namibia, exploration continues at the Lofdal rare earths project in the Kunene region on mineralisation that holds a fairly high proportion of the more valuable heavy REE.

The project company, Namibia Rare Earths, recently applied for a mining licence, stating: ‘While difficult market conditions for the resource sector in general, and rare earths in particular, persist, Lofdal remains a unique opportunity for a sustainable supply of heavy rare earths outside China.’

In South Africa, work continues at the Zandkopsdrift project in the Namaqualand region of the Northern Cape province, operated by Frontier Rare Earths. But the company has run into difficulties. It delisted from the Toronto Stock Exchange in 2015, and continues to sound serious notes of caution in its quarterly updates – recently stating that ‘a doubling of rare earth prices from current levels would still produce a negative net present value for the Zandkopsdrift project’.

In the country’s Limpopo province, the Glenover project may yet produce REE – notably scandium – as a cost-effective byproduct of phosphate mining.

Further north, analysts continue to call attention to the Songwe Hill project in Malawi, run by Canada’s Mkango Resources. Here, a combination of REE-bearing minerals may offer the chance to recover the best of the light and heavy rare earths. The company has sounded a relatively positive note in recent management discussions, arguing that an updated prefeasibility study, published in November 2015, continues to suggest the viability and future value of Songwe Hill, with relatively low capital expenditure required to develop an open-pit operation.

In Tanzania, Australia-listed Peak Resources is currently completing a bankable feasibility study for the expansive Ngualla project, identified at its discovery as one of the largest undeveloped REE deposits outside of China. After updating its assumptions in May 2016, Peak also remains positive, given the low radioactivity, low strip ratio and high volumes of neodymium and praseodymium – both vital for magnet manufacture – in its deposit. The company expects to receive a mining licence in 2017, and anticipates the commissioning of a 31-year open-pit mine, producing 28 000 tons of 45% rare earth concentrate per year.

Projects such as Ngualla are some of the most promising in Africa at present. But for all rare-earths producers, the future looks no more certain than it did a year ago. Part of the problem is that analysts and investors don’t have a clear picture of the market. The range of potential REE applications is vast, making it hard to anticipate demand. The possibility of China shifting its policy or ramping up production – again jeopardising projects internationally – continues to cast a shadow over all prospective projects. Technological innovation in key areas may also reduce demand.

As REE expert Jon Hykawy recently observed in an interview with Investing News Network: ‘The rare earth recovery that a lot of people have been hoping for hasn’t been happening. There are a number of reasons for that, not least of which is that a lot of the industrial consumers of rare earths, especially magnet materials, have been avoiding their use… Companies like Chevrolet and General Motors are actively coming out and saying, “We are de-emphasising rare earth use”.’

Current uncertainties about supply have constrained demand, and when projects turn into mines, there are other challenges to overcome: processing, environmental risks and equitable supply chains.

However, in an increasingly high-tech world, most analysts predict a rising demand for rare earths in the medium term, and particularly for neodymium, praseodymium and dysprosium. Several African projects host high proportions of these elements, and may have the chance to capture some of China’s market share.